Key Takeaways: DeFi APY vs APR in 2026

- APR = simple interest (no compounding). APY = effective yield after compounding. The formula is

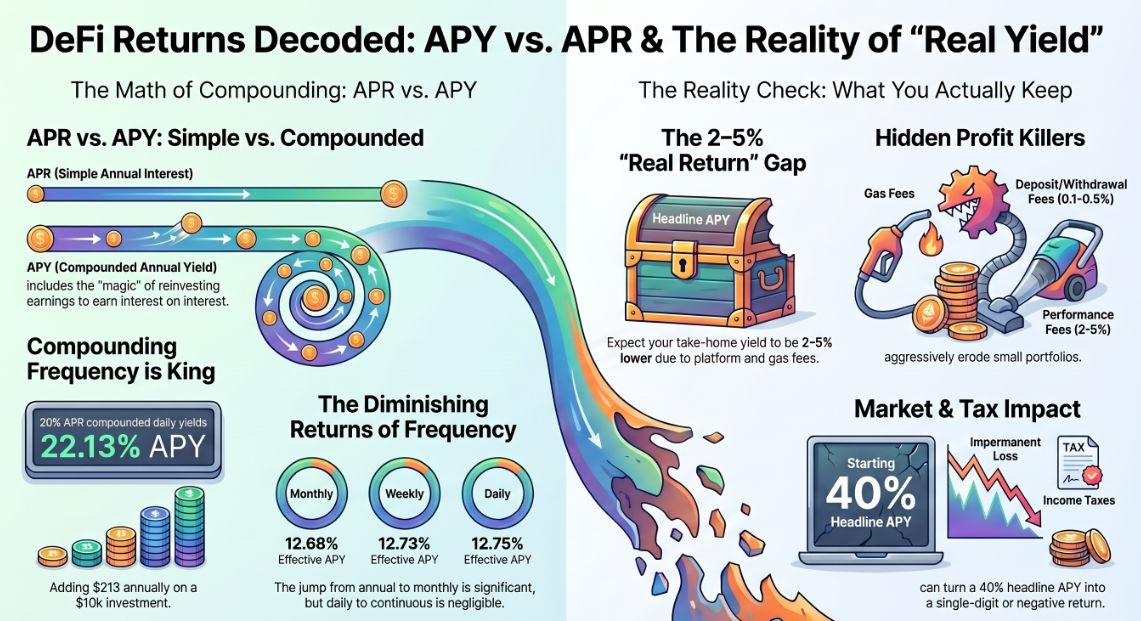

APY = (1 + APR/n)^n − 1, where n is the number of compounding periods per year. - A 20% APR compounded daily becomes roughly 22.13% APY — a 2.13 percentage-point jump that scales with your balance.

- Your real DeFi return is typically 2–5% lower than the headline APY once you subtract platform fees, gas, impermanent loss, and taxes.

- Most DeFi front-ends advertise APY to look bigger; most lending protocols (e.g. Aave, Compound) quote supply APR that auto-compounds into APY on-chain.

- Use L2s (Polygon, Arbitrum, Optimism) to compound cheaply and auto-compounders like Beefy Finance or Yearn to squeeze every basis point out of your position.

Understanding the Difference Between APY and APR in DeFi

Look, I’ll be honest with you. When I first started exploring DeFi platforms, I thought APY and APR were basically the same thing with different letters. Boy, was I wrong! That confusion cost me a few hundred bucks in missed earnings because I didn’t understand how compounding actually worked.

Here’s the deal: APR (Annual Percentage Rate) is the simple interest rate you earn over a year without any compounding. It’s straightforward – if you invest $1,000 at 10% APR, you’ll earn $100 in a year, period. APY (Annual Percentage Yield), on the other hand, includes the magic of compound interest. That same 10% can turn into 10.47% APY if it compounds daily!

The difference might seem small at first glance, but trust me, it adds up fast. I remember staking some ETH on a DeFi lending platform advertising 12% returns, and I didn’t bother checking whether it was APY or APR. Turns out it was APR with monthly compounding, which meant my actual yield was closer to 12.68% APY. That extra 0.68% on a $5,000 investment meant an additional $34 in my pocket by year’s end.

The Math Behind APY vs APR

Let me break down the actual formula because understanding this changed everything for me. APY is calculated using this formula: APY = (1 + r/n)^n – 1, where r is the APR and n is the number of compounding periods per year. (See Investopedia’s primer on compound interest if you want the traditional-finance version.)

So if you’ve got a 20% APR that compounds daily (365 times per year), your APY would be: (1 + 0.20/365)^365 – 1 = 0.2213 or 22.13% APY. That’s a 2.13% difference just from compounding! On a $10,000 investment, that’s an extra $213 annually.

Most DeFi yield farming platforms compound your rewards automatically, which is why they advertise APY instead of APR. But here’s where it gets tricky – some platforms show APR and let you manually compound, while others auto-compound and show APY. You gotta know which one you’re looking at.

How Compounding Frequency Affects Your Real Returns

This is where things get really interesting. The frequency of compounding makes a massive difference in your actual returns, and I learned this the hard way when comparing two yield farming platforms.

Platform A offered 15% APR with weekly compounding. Platform B offered 14.5% APR with daily compounding. At first, I went with Platform A because 15% is bigger than 14.5%, right? Wrong! When I actually calculated the APY, Platform A gave me 16.08% APY, while Platform B delivered 15.56% APY. Okay, so Platform A was still better, but not by as much as I thought.

Here’s a quick breakdown of how different compounding frequencies affect a 12% APR:

- Annual compounding: 12% APY (no difference)

- Monthly compounding: 12.68% APY

- Weekly compounding: 12.73% APY

- Daily compounding: 12.75% APY

- Continuous compounding: 12.75% APY (theoretical maximum)

The jump from annual to monthly is huge (0.68%), but the difference between daily and continuous is basically nothing. That’s why most DeFi protocols stick with daily compounding – it’s close enough to the maximum without being computationally expensive.

Gas Fees Can Kill Your Compounding Strategy

Here’s something nobody talks about enough: gas fees can completely wreck your compounding returns, especially on Ethereum mainnet. I was using a yield farming protocol that required manual claiming and restaking of rewards. The APR was advertised at 25%, which sounded amazing!

But every time I wanted to compound my earnings, I had to pay gas fees. During peak times, those fees could be $50-100 per transaction. If I was earning $200 per week and wanted to compound weekly, I’d lose $50 to gas fees – that’s 25% of my earnings gone! My effective APY dropped from the theoretical 28.39% (with weekly compounding) down to maybe 20% after accounting for gas costs.

That’s when I switched to platforms with auto-compounding features or moved to Layer 2 solutions like Polygon and Arbitrum where gas fees are pennies instead of dollars. On Polygon, I can compound daily without worrying about fees eating into my profits.

Calculating Your Real Returns: A Step-by-Step Guide

Alright, let’s get practical. I’m gonna walk you through exactly how I calculate my real DeFi returns, accounting for all the hidden factors that most people ignore.

First, you need to know your starting investment amount and the advertised rate. Let’s say you’re putting $5,000 into a liquidity pool offering 18% APR with daily compounding. Step one is converting that APR to APY using the formula I mentioned earlier. With daily compounding, 18% APR becomes 19.72% APY.

But wait – we’re not done yet! You also need to factor in:

- Deposit fees (some platforms charge 0.1-0.5% to enter a pool)

- Withdrawal fees (usually 0.1-0.5% when you exit)

- Performance fees (many platforms take 2-5% of your earnings)

- Gas fees for claiming and compounding

- Impermanent loss if you’re in a liquidity pool

Let’s say your platform charges a 0.3% deposit fee, 0.3% withdrawal fee, and takes 4% of your earnings as a performance fee. On your $5,000 investment at 19.72% APY, here’s what actually happens:

You deposit $5,000 but lose $15 to the deposit fee, so you’re starting with $4,985. Over the year, you’d earn $983 (19.72% of $4,985). But the platform takes 4% of that ($39), leaving you with $944 in earnings. When you withdraw your $5,929, you lose another 0.3% ($18) to the withdrawal fee.

Your actual profit: $5,911 – $5,000 = $911. That’s an effective return of 18.22%, not the advertised 19.72% APY. Still good, but you can see how fees add up!

Using DeFi Calculators and Tracking Tools

I used to track everything manually in a spreadsheet, and honestly, it was a pain. Now I use tools like DeFi Llama and Zapper to monitor my positions across multiple platforms. These tools automatically calculate your real returns including fees and show you exactly how much you’re earning.

There are also specific APY calculators online where you can input the APR, compounding frequency, and time period to see your expected returns. I use these before entering any position to make sure the math actually makes sense.

One tool I really like is the impermanent loss calculator on DailyDefi.org. If you’re providing liquidity to a pool with two assets (like ETH/USDC), you need to account for potential impermanent loss. I’ve had situations where I earned 20% APY from fees but lost 15% to impermanent loss because ETH’s price moved significantly. My net return was only 5%!

Common Mistakes When Calculating DeFi Returns

Let me share some of the biggest mistakes I’ve made (and seen others make) when calculating DeFi returns. These errors can make you think you’re earning way more than you actually are.

Mistake #1: Ignoring token price volatility. If you’re earning rewards in the platform’s native token, you need to account for price changes. I once earned 50% APY in a governance token, but the token’s price dropped 60% during that time. My actual return in dollar terms was negative!

Mistake #2: Not accounting for impermanent loss in liquidity pools. This is huge. When you provide liquidity to a pool like ETH/DAI, you’re exposed to impermanent loss if the price ratio changes. I’ve seen people celebrate their 30% APY from trading fees while ignoring the 25% impermanent loss they suffered.

Mistake #3: Forgetting about taxes. In most countries, DeFi earnings are taxable events. Every time you claim rewards, that’s taxable income. Every time you compound, that might be a taxable event too. I learned this the hard way when tax season came around and I owed way more than I expected.

The Reality Check: What Returns Are Actually Achievable?

Here’s some real talk based on my experience across different DeFi platforms. Sustainable, relatively safe returns in DeFi typically range from 3-8% APY on stablecoins and 5-15% APY on major cryptocurrencies like ETH and BTC.

If someone’s advertising 100% APY or higher, there’s usually a catch. Either the rewards are paid in a highly inflationary token that’s losing value, or the platform is using unsustainable incentives that’ll dry up soon. I’ve chased those high yields before, and more often than not, I ended up with less money than I started with.

The sweet spot I’ve found is platforms offering 8-15% APY on stablecoins with proven track records and audited smart contracts. These returns are significantly better than traditional savings accounts (which offer maybe 0.5-1%) but aren’t so high that they’re obviously unsustainable.

Advanced Strategies for Maximizing Your Real Returns

Once you understand the basics of APY vs APR and how to calculate real returns, you can start implementing strategies to maximize your earnings. These are tactics I’ve developed over time that have significantly improved my DeFi returns.

Strategy #1: Auto-compounding vaults. Instead of manually claiming and restaking rewards, use platforms like Beefy Finance or Yearn that automatically compound your earnings multiple times per day. This maximizes your APY without you having to pay gas fees for each compound.

Strategy #2: Layer 2 solutions for smaller portfolios. If you’re working with less than $10,000, Ethereum mainnet gas fees will eat you alive. I moved most of my smaller positions to Polygon, Arbitrum, and Optimism where I can compound daily for pennies in gas fees.

Strategy #3: Use auto-compounders like Beefy Finance and Yearn so your rewards reinvest automatically and you capture the full APY without paying gas every day. Strategy #4: Diversification across platforms and chains. Don’t put all your eggs in one basket. I spread my funds across 4-5 different platforms and 2-3 different chains. This reduces my risk if one platform gets hacked or one chain has issues.

Monitoring and Adjusting Your Positions

The DeFi landscape changes fast. A pool offering 20% APY today might drop to 8% APY next month as more liquidity enters. I check my positions at least once a week to make sure the returns are still competitive.

I also set alerts using tools like DeFi Pulse to notify me when APYs drop below certain thresholds. If a position falls below 10% APY, I’ll usually move those funds to a better opportunity. The key is staying active and not just setting and forgetting.

One thing I track religiously is my effective APY after all fees and losses. I maintain a spreadsheet where I log my actual returns every month. This helps me identify which platforms and strategies are actually working versus which ones just look good on paper.

Tax Implications of DeFi Returns

Disclaimer: The following is general information based on personal experience, not tax advice. DeFi tax rules vary by jurisdiction and change frequently. Please consult a qualified tax professional or accountant before making decisions about your own situation.

Okay, this isn’t the fun part, but it’s super important. Every time you earn rewards in DeFi, that’s taxable income in most jurisdictions. And the tax situation can get complicated fast.

When you claim rewards, you owe income tax on the fair market value of those tokens at the time you received them. If you then sell those tokens later at a higher price, you also owe capital gains tax on the difference. If you sell at a lower price, you can claim a capital loss.

I use tools like Koinly and CoinTracker to automatically track all my DeFi transactions and calculate my tax liability. These tools connect to your DeFi wallets and exchanges and generate tax reports that you can give to your accountant. Trust me, trying to do this manually is a nightmare.

Here’s a real example from my own taxes: I earned $5,000 in DeFi rewards throughout the year. That $5,000 was taxed as ordinary income at my marginal tax rate (let’s say 24%), so I owed $1,200 in taxes. But I also had to pay capital gains tax on any appreciation of those tokens before I sold them. My effective return after taxes was significantly lower than the advertised APY.

Strategies for Tax-Efficient DeFi Investing

There are some strategies you can use to minimize your tax burden. One approach is to hold your DeFi positions for at least a year before selling, which qualifies you for long-term capital gains rates (usually lower than ordinary income rates).

Another strategy is tax-loss harvesting. If you have positions that are down, you can sell them to realize the loss and offset your gains from other positions. I do this at the end of every year to reduce my overall tax liability.

Some people also use retirement accounts like self-directed IRAs to invest in DeFi, which allows your earnings to grow tax-deferred or even tax-free (in the case of Roth IRAs). I haven’t personally done this yet, but it’s something I’m exploring for long-term DeFi holdings.

Conclusion: Making Informed Decisions About DeFi Returns

Understanding the difference between APY and APR is just the starting point. To truly calculate your real DeFi returns, you need to account for compounding frequency, fees, gas costs, impermanent loss, token price volatility, and taxes. It’s a lot to keep track of, but it’s essential if you want to make informed investment decisions.

The advertised APY on a DeFi platform is rarely what you’ll actually earn. In my experience, your real returns are usually 2-5% lower after accounting for all the factors I’ve discussed. That doesn’t mean DeFi isn’t worth it – even with all the fees and complications, you can still earn significantly more than traditional savings accounts or bonds.

The key is to go into every DeFi investment with your eyes wide open. Use calculators, track your actual returns, and don’t be afraid to move your funds if a platform isn’t delivering the returns you expected. DeFi is still a relatively new space, and the platforms that offer the best risk-adjusted returns today might not be the same ones offering the best returns tomorrow.

Start small, learn the ropes, and gradually increase your positions as you get more comfortable with calculating and maximizing your real returns. And remember – if something seems too good to be true (like 500% APY), it probably is. Stick with established platforms, do your research, and always prioritize security over chasing the highest yields.

What’s your experience with calculating DeFi returns? Have you found any tools or strategies that work particularly well? Drop a comment below and share your insights – I’m always looking to learn from other people’s experiences in this space!

Frequently Asked Questions: DeFi APY vs APR

Is APY always higher than APR in DeFi?

Yes, as long as there is any compounding (daily, weekly, monthly) APY will be higher than APR. The only case where APY equals APR is when compounding happens exactly once per year — essentially never in DeFi.

Why do DeFi protocols show both a supply APR and a supply APY?

Protocols like Aave and Compound pay interest block-by-block, so the “raw” rate they earn is an APR. Because that interest is continuously re-added to your balance on-chain, the effective annualized return you actually receive is the APY — which is why both numbers appear on dashboards.

What is the APY formula I can use in a spreadsheet?

Use: APY = (1 + APR/n)^n - 1. In Excel or Google Sheets: =(1+A1/B1)^B1-1, where A1 is the APR (as a decimal) and B1 is the number of compounding periods per year (365 for daily, 52 for weekly, 12 for monthly).

Do gas fees reduce my effective APY?

Absolutely. Every time you claim or compound rewards manually on Ethereum mainnet, gas costs are subtracted from your gross earnings. On L2s like Polygon, Arbitrum, and Optimism the drag is usually negligible, which is why small accounts should compound there or use auto-compounders like Beefy Finance or Yearn.

Is a higher APY always better?

No. Very high APYs (500%+) typically come from new tokens with heavy emissions, low liquidity, or undisclosed smart-contract risk. Your risk-adjusted return matters more than the headline number. A stable 6–12% APY on an audited blue-chip protocol usually beats a volatile 200% APY that rug-pulls.

How does impermanent loss affect real APY in liquidity pools?

Impermanent loss is the gap between holding two tokens versus supplying them to an AMM pool when their prices diverge. It directly reduces the APY you see — a pool advertising 40% APY can easily net only 15–20% once IL is accounted for during volatile weeks.

Should I pick the platform with the highest APY?

Not by itself. Weigh APY against audit history, TVL, track record, chain gas costs, fees, and IL exposure. Our guides on the best DeFi lending platforms, best yield farming platforms, and best DeFi wallets for staking walk through that trade-off in detail.