Here’s a wild stat that still blows my mind: over $50 billion is currently locked in DeFi protocols, and a good chunk of that is regular folks like you and me earning passive income on their crypto. When I first stumbled into the world of decentralized finance back in 2021, I honestly thought it was some kind of scam. Turns out, I was just intimidated by all the jargon!

Look, I get it. The whole DeFi thing can seem overwhelming at first. Yield farming? Liquidity pools? APY vs APR? It’s like learning a new language. But here’s the thing – once you understand the basics, earning passive crypto income becomes way less scary than it sounds. And trust me, I’ve made plenty of mistakes along the way so you don’t have to.

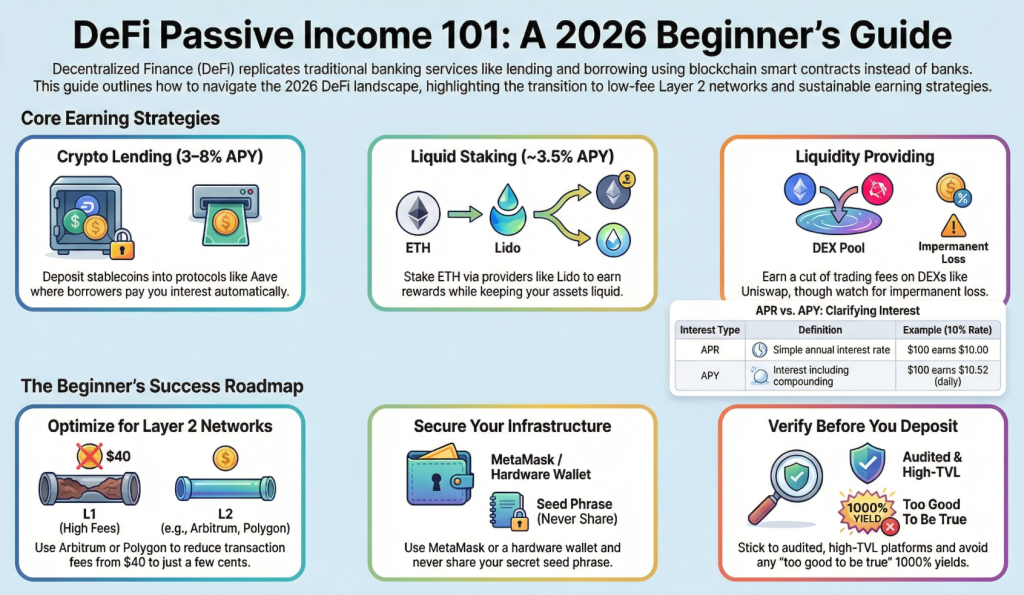

In short, you can earn passive income with DeFi by lending crypto on platforms like Aave (3–8% APY), staking ETH via Lido (~3.5% APY), or providing liquidity on decentralized exchanges like Uniswap. You can start with as little as $200 on a Layer 2 network like Arbitrum to minimize gas fees.

In this guide, I’m gonna break down everything you need to know about earning passive income through DeFi in 2026. No fancy finance degree required. Just real talk about what works, what doesn’t, how to get started and how to earn passive income with DEFI even if you only have a couple hundred bucks to play with.

What Exactly Is DeFi and Why Should You Care?

DeFi stands for decentralized finance, and it’s basically a way to do all the stuff banks do – lending, borrowing, earning interest – but without the actual banks. Instead, everything runs on smart contracts on blockchains like Ethereum, Polygon, or Arbitrum. Pretty cool, right?

The reason I got excited about DeFi was the interest rates. My savings account at the bank was paying me like 0.5% APY. Meanwhile, I was seeing DeFi platforms offering 5%, 10%, sometimes even higher returns on stablecoins. Now, I’ll be honest – those crazy high yields from a few years ago have come down quite a bit. But you can still earn significantly more than traditional banks offer.

What makes DeFi different is that you’re always in control of your funds. There’s no bank that can freeze your account or tell you what to do with your money. Your crypto sits in your own wallet, and you decide when to deposit or withdraw. It’s financial freedom in the truest sense.

The Main Ways Of How to Earn Passive Income With DeFi

Alright, let’s get into the meat of this. There’s a few different strategies for generating passive crypto income, and each one has its own risk-reward profile. I’ve tried most of these myself, so I can tell you what actually works.

Crypto Lending

Crypto lending is probably the simplest way to start. You deposit your crypto into a lending protocol like Aave or Compound, and borrowers pay interest to use it. The platform handles everything automatically through smart contracts. Current rates for stablecoins like USDC or DAI hover around 3-8% APY depending on market conditions. Not life-changing, but way better than my Chase savings account.

Liquidity Providing

Liquidity providing is where things get more interesting – and more risky. You provide pairs of tokens to decentralized exchanges like Uniswap or SushiSwap, and you earn a cut of the trading fees. The returns can be higher, but there’s this thing called impermanent loss that can eat into your profits if token prices move a lot. More on that later.

Staking

Staking is another popular option. With protocols like Lido or Rocket Pool, you can stake your ETH and earn around 3-4% annually while supporting the Ethereum network. It’s relatively low risk compared to other DeFi strategies. I’ve got a portion of my portfolio in staked ETH and it just sits there quietly accumulating rewards.

Yield Farming

Yield farming combines multiple strategies to maximize returns. You might lend out crypto, get a receipt token, then stake that token somewhere else for additional rewards. It can get complicated fast, but the yields can also be substantial for those willing to put in the work.

How Much Money Do You Actually Need to Start?

This is probably the most common question I get, and the answer might surprise you. You can technically start with as little as $50, but here’s the catch – gas fees can absolutely wreck you if you’re working with small amounts.

Back when I was just getting started, I tried to deposit $100 into a lending protocol on Ethereum mainnet. The gas fee was like $40. That’s 40% of my investment gone just to make one transaction! I learned real quick that timing and network choice matter a lot.

My honest recommendation? If you’re on Ethereum mainnet, you probably want at least $1,000 to make the gas fees worthwhile. But here’s the good news – Layer 2 networks like Polygon, Arbitrum, and Optimism have changed the game completely. Gas fees there are often just a few cents. You can realistically start DeFi on these networks with $200-$500 and not feel like you’re bleeding money on transactions.

I actually do most of my DeFi activity on Arbitrum now. Same protocols, way cheaper fees. It’s been a game changer for smaller portfolios.

Understanding APY vs APR (This Confused Me for Months)

Okay, confession time. I spent way too long not understanding the difference between APY and APR, and it cost me some potential earnings. Let me save you the headache.

APR (Annual Percentage Rate) is the simple interest rate. If a protocol shows 10% APR, you’d earn roughly 10% over a year on your initial deposit. Straightforward enough.

APY (Annual Percentage Yield) accounts for compound interest. When your rewards get added to your principal and start earning their own rewards, that’s compounding. A 10% APR with daily compounding actually works out to about 10.52% APY. The more frequently compounding happens, the bigger the difference.

Here’s why this matters: some protocols show APR, others show APY, and some shady ones switch between them to make their rates look better. Always check which one you’re looking at. A platform advertising 100% APR sounds similar to 100% APY, but the actual returns can be quite different depending on compounding frequency.

Pro tip: auto-compounding vaults like those on Yearn Finance or Beefy Finance handle compounding automatically. They’ll harvest your rewards and reinvest them for you, which saves you gas fees and maximizes your effective APY. I use these a lot because I’m lazy and don’t want to manually claim and restake every day.

The Real Risks You Need to Know About

I’d be doing you a disservice if I didn’t talk about the risks involved with DeFi. This isn’t a guaranteed money printer, and I’ve seen people lose significant amounts by ignoring red flags.

Smart Contract Risk

Smart contract risk is the big one. These protocols run on code, and code can have bugs. Even audited contracts have been exploited before. The 2022 Ronin bridge hack saw $625 million stolen. That’s not me trying to scare you – it’s just reality. Stick to well-established protocols with multiple audits and long track records.

Impermanent Loss

Impermanent loss affects liquidity providers specifically. If you provide liquidity for an ETH/USDC pair and ETH price doubles, you would’ve been better off just holding the ETH. The math gets complicated, but basically – volatile token pairs can result in losses compared to simply holding. I learned this the hard way during a bull run.

Protocol Risk

Protocol risk is another factor. Even legitimate projects can fail. The team might abandon development, the token price might crash, or regulatory issues could arise. Diversifying across multiple protocols helps manage this risk.

Rug Pulls and Scams

Rug pulls and scams unfortunately still exist in DeFi. If something promises 1000% APY, it’s probably too good to be true. Anonymous teams, unaudited contracts, and aggressive marketing are all red flags. I always check DeFiLlama and do some basic research before depositing anywhere new.

Getting Started: A Simple Step-by-Step Approach

Alright, enough theory. Let’s talk about actually doing this. Here’s how I’d recommend a complete beginner get started on how to earn passive income with DEFI.

Step 1: Get a proper wallet. Download MetaMask or use a hardware wallet like Ledger if you’re dealing with significant amounts. Write down your seed phrase and store it somewhere safe. I cannot stress this enough – lose your seed phrase and you lose everything.

Step 2: Fund your wallet. Buy some crypto on an exchange like Coinbase or Kraken, then withdraw it to your wallet. I’d suggest starting with a stablecoin like USDC plus some ETH or MATIC for gas fees.

Step 3: Bridge to Layer 2 (optional but recommended). If gas fees on Ethereum mainnet are high, use the official bridge to move funds to Arbitrum, Optimism, or Polygon. This’ll save you money on future transactions.

Step 4: Start with lending. Go to Aave, connect your wallet, and deposit your stablecoin. That’s literally it. You’re now earning interest in DeFi. The interface is pretty user-friendly these days.

Step 5: Explore and learn. Once you’re comfortable with basic lending, you can branch out into liquidity providing, yield farming, or staking. Take your time. There’s no rush.

My Top Platform Recommendations for 2026

After years of using various DeFi protocols, here are the ones I personally trust and use regularly.

Aave

Aave is my go-to for lending. It’s been around since 2017, has billions in TVL, multiple audits, and operates on most major chains. The interface is clean and the rates are competitive. Can’t go wrong here for beginners.

Lido

Lido is where I stake my ETH. They’re the largest liquid staking provider, and you get stETH tokens that you can use elsewhere in DeFi while still earning staking rewards. Current ETH staking yields around 3.5% APY.

Uniswap

Uniswap remains the king of decentralized exchanges. If you want to provide liquidity, their V3 concentrated liquidity feature lets you earn more fees with less capital. Just be careful with volatile pairs.

Beefy Finance

Beefy Finance is great for auto-compounding. They aggregate yield opportunities across dozens of chains and handle all the compounding for you. I use them for some of my more passive positions.

Curve Finance

Curve Finance specializes in stablecoin swaps and has some of the best rates for stablecoin liquidity providing. Lower risk of impermanent loss since you’re dealing with assets that should stay similarly priced.

Don’t Forget About Taxes

I know, I know – nobody wants to think about taxes. But DeFi income is taxable in most jurisdictions, and the IRS has been cracking down on crypto reporting. Every time you earn interest, claim rewards, or swap tokens, that’s potentially a taxable event.

I use a crypto tax software like Koinly to track all my DeFi transactions. It connects to your wallets and exchanges, imports everything, and generates tax reports. Worth every penny to avoid a headache (or audit) come tax season.

Keep records of everything – deposits, withdrawals, rewards claimed, tokens swapped. Your future self will thank you when you’re not trying to reconstruct a year’s worth of on-chain activity from etherscan.

Final Thoughts: Is DeFi Passive Income Worth It?

After several years in DeFi, my honest answer is yes – but with caveats. It’s not “set it and forget it” like a savings account. You need to stay informed, manage risks, and occasionally rebalance your positions. The yields have normalized from the crazy early days, but they still beat traditional finance for those willing to learn.

Start small. Use only money you can afford to lose while you’re learning. Stick to established protocols. And don’t chase ridiculous APYs – if it looks too good to be true, it probably is.

The DeFi space is constantly evolving. New protocols launch, old ones improve, and the whole ecosystem keeps getting more user-friendly. 2026 is honestly a great time to get started because the infrastructure has matured significantly. Gas fees are lower than ever on L2s, interfaces are cleaner, and there’s way more educational content available.

I’d love to hear about your DeFi journey! Drop a comment below with your questions or share your own experiences. What protocols are you using? What challenges have you faced? Let’s learn from each other.