Did you know that the global DeFi lending market surpassed $50 billion in total value locked in early 2026? That’s not a typo. Fifty. Billion. Dollars. (You can track live figures on DeFiLlama’s lending dashboard.) Sitting in decentralized lending protocols, earning interest for everyday people like you and me — no bank required. When I first stumbled onto DeFi lending back in the day, I honestly thought it was too good to be true. Spoiler: it’s not, but you do need to know what you’re doing.

Did you know that the global DeFi lending market surpassed $50 billion in total value locked in early 2026? That’s not a typo. Fifty. Billion. Dollars. (You can track live figures on DeFiLlama’s lending dashboard.) Sitting in decentralized lending protocols, earning interest for everyday people like you and me — no bank required. When I first stumbled onto DeFi lending back in the day, I honestly thought it was too good to be true. Spoiler: it’s not, but you do need to know what you’re doing.

I’ve spent years testing, losing a little, winning a lot, and learning the hard way which DeFi lending platforms are actually worth your time and money. And in 2026, the landscape has matured significantly. There are clear winners, some solid mid-tier options, and a few platforms you should probably avoid unless you enjoy stress-eating at 2am watching your funds drain into a hack.

In this guide, I’m ranking the best DeFi lending platforms by interest rates, safety, ease of use, and overall value. Whether you’ve got $200 or $200,000 to put to work, there’s something here for you. Let’s get into it.

Key Takeaways: Best DeFi Lending Platforms in 2026

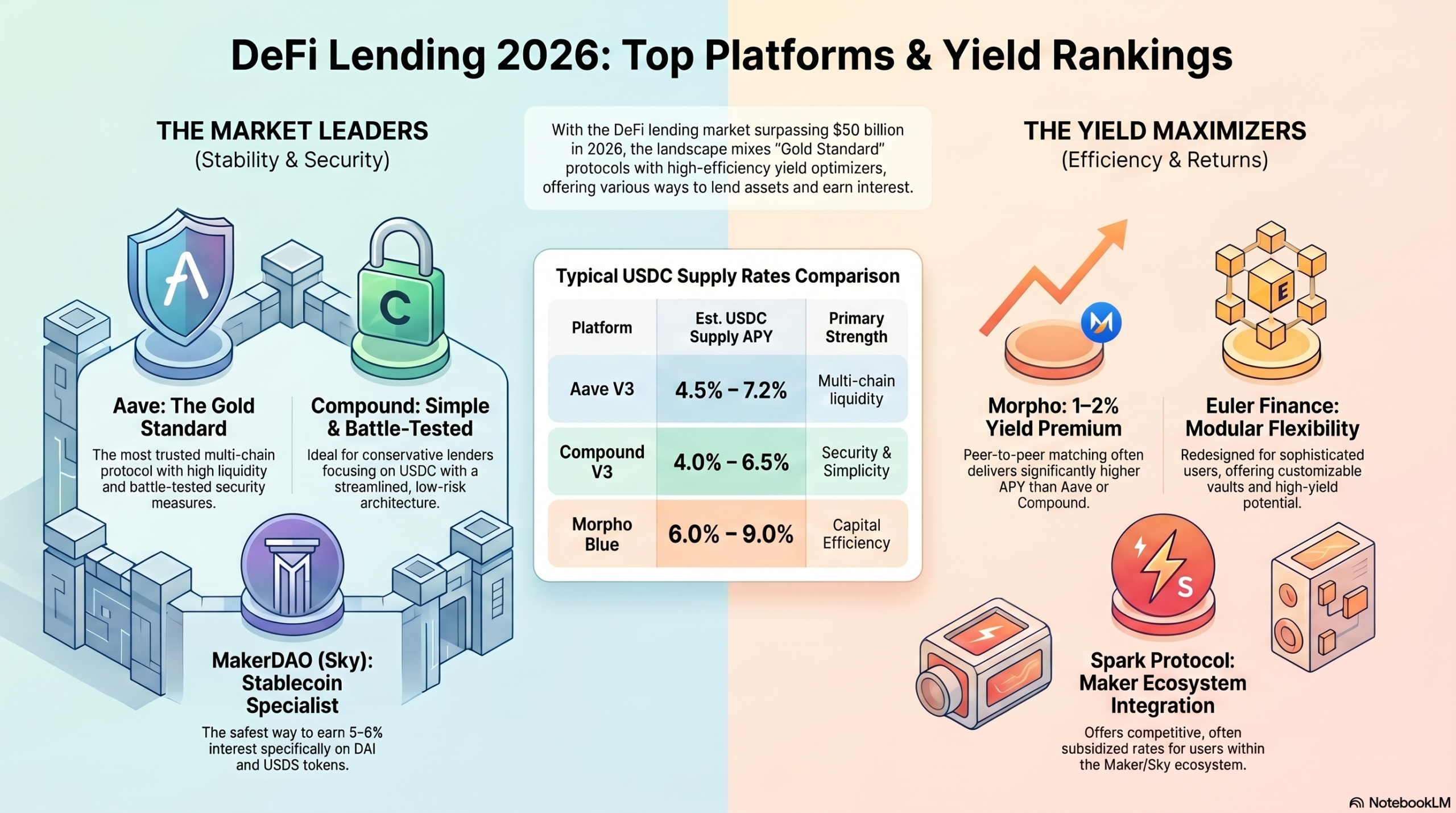

- Best overall: Aave — the gold standard for security, liquidity, and multi-chain support.

- Highest stablecoin yield: Morpho — often 1–2% higher APY on USDC than Aave or Compound.

- Most battle-tested: Compound — the protocol that started DeFi lending, still rock-solid.

- Best for DAI / USDS holders: MakerDAO / Sky Protocol — earn directly on the stablecoin you already hold.

- Start small: $100–$200 is enough to learn the ropes; never deposit funds you can’t afford to lose.

What Is DeFi Lending and Why Should You Care?

DeFi lending is basically what it sounds like — lending your crypto to borrowers through a decentralized protocol and earning interest in return. No bank. No middleman. No waiting three business days for anything. The smart contract handles everything automatically, 24/7, 365 days a year.

Here’s the thing that blew my mind when I first got into this: traditional savings accounts were paying something like 0.01% APY at most banks. Meanwhile, DeFi lending platforms were offering 5%, 8%, even 12% on stablecoins. That’s not a rounding error — that’s a fundamentally different financial system.

The way it works is pretty elegant. You deposit your crypto (say, USDC or ETH) into a lending pool. Borrowers come along, put up collateral (usually more crypto than they’re borrowing — this is called overcollateralization), and take out a loan. The interest they pay flows back to you, the lender. Simple in concept, but the execution varies wildly between platforms.

How We Ranked These DeFi Lending Platforms

Before I just throw a list at you, let me explain how I evaluated these platforms. Because “highest APY” is not the only thing that matters — trust me, I learned that the hard way after chasing yield on a sketchy protocol that got exploited.

- Interest rates (APY): Both supply rates for lenders and borrow rates for borrowers

- Security and audit history: Has the smart contract been audited? Any past exploits?

- Total Value Locked (TVL): Higher TVL generally means more trust and liquidity

- Supported assets: How many tokens can you lend or borrow?

- Network availability: Ethereum mainnet, Layer 2s, or multi-chain?

- User experience: Is the interface actually usable for a normal human being?

- Governance and decentralization: Who controls the protocol?

I also factored in real user feedback and my own hands-on experience. These aren’t just theoretical rankings — I’ve actually used most of these platforms with real money.

#1 Aave — The Gold Standard of DeFi Lending

If DeFi lending had a Mount Rushmore, Aave would be front and center. This protocol has been around since 2017 (originally as ETHLend), and it’s survived multiple market cycles, countless hacks on other platforms, and the general chaos of crypto. That kind of track record matters.

As of 2025, Aave V3 is the dominant version, and it’s genuinely impressive. You can lend and borrow across Ethereum, Polygon, Arbitrum, Optimism, Avalanche, and more. The multi-chain support alone makes it incredibly flexible. I personally use Aave on Arbitrum because the gas fees are a fraction of Ethereum mainnet — we’re talking cents instead of dollars.

Current APY ranges on Aave (approximate, as of early 2025):

- USDC: 4.5% – 7.2% supply APY

- USDT: 4.1% – 6.8% supply APY

- ETH: 1.8% – 3.5% supply APY

- WBTC: 0.5% – 1.2% supply APY

The rates fluctuate based on utilization — when more people are borrowing, lenders earn more. It’s a dynamic interest rate model, and honestly it’s pretty smart. Aave also has a Safety Module where AAVE token holders stake their tokens as insurance against shortfall events. That’s a real layer of protection you don’t see everywhere.

One thing I love about Aave is the “E-Mode” feature in V3. If you’re lending and borrowing correlated assets (like ETH and stETH), you can unlock higher capital efficiency. It’s a bit advanced, but once you understand it, it’s a game-changer for maximizing returns.

Verdict: Best overall DeFi lending platform. Highest trust, solid rates, multi-chain, and battle-tested security. Start here if you’re new to DeFi lending.

#2 Compound — The Protocol That Started It All

Compound is basically the grandfather of DeFi lending. It launched in 2018 and pioneered the concept of algorithmic interest rates and liquidity mining. Without Compound, a lot of what we know as DeFi today wouldn’t exist. I have a soft spot for it, honestly.

Compound V3 (also called Comet) made some significant changes from V2. The biggest shift is that V3 focuses on a single base asset per market — currently USDC on Ethereum and Arbitrum. This is actually a security improvement because it reduces the attack surface. Simpler architecture means fewer things that can go wrong.

Current APY on Compound V3 (approximate):

- USDC supply APY: 4.0% – 6.5%

- USDC borrow APY: 5.5% – 8.0%

The COMP token rewards can boost your effective yield if you’re actively participating in governance. I’ve earned a decent chunk of COMP over the years just by being a lender — it’s like a loyalty bonus on top of your interest.

Where Compound falls slightly behind Aave is in asset variety and chain support. It’s more limited in scope, which some people actually prefer — less complexity, less risk. If you’re a “keep it simple” type of investor, Compound might actually be your jam.

Verdict: Excellent for USDC lending specifically. Slightly lower rates than Aave in some cases, but rock-solid security and a proven track record. Great for conservative DeFi lenders.

#3 MakerDAO / Sky Protocol — Earn on DAI and USDS

MakerDAO is a bit different from Aave and Compound. Rather than being a pure lending marketplace, Maker is the protocol that creates DAI — the decentralized stablecoin. But they also offer the DAI Savings Rate (DSR), which lets you earn interest just by depositing DAI into the Maker protocol.

In 2024, MakerDAO rebranded to Sky Protocol and introduced USDS as an upgraded version of DAI. The Sky Savings Rate (SSR) has been competitive, often sitting in the 5-8% range depending on governance decisions. It’s one of the simplest ways to earn yield in DeFi — deposit DAI or USDS, earn interest, withdraw anytime.

What I appreciate about Maker is the transparency. Every parameter — the savings rate, collateral ratios, stability fees — is set by MKR/SKY token holders through on-chain governance. You can literally watch the votes happen in real time. That level of transparency is rare and valuable.

The downside? You’re limited to DAI/USDS. If you want to lend ETH or WBTC, you need to go elsewhere. But for stablecoin yield specifically, the DSR/SSR is one of the safest options in all of DeFi.

Verdict: Best for DAI/USDS holders who want simple, safe stablecoin yield. Not the highest rates, but extremely reliable and transparent.

#4 Morpho — The Yield Optimizer That’s Quietly Crushing It

Okay, this one might be new to some of you, and that’s exactly why I’m excited to talk about it. Morpho has been one of the most interesting developments in DeFi lending over the past couple of years. It started as a peer-to-peer layer on top of Aave and Compound, matching lenders and borrowers directly to give both sides better rates.

Morpho Blue (the current version) is a standalone lending protocol that’s incredibly capital efficient. The rates are often noticeably better than Aave or Compound for the same assets. I’ve personally seen USDC supply rates on Morpho run 1-2% higher than on Aave during certain periods. That adds up fast when you’re talking about significant capital.

Why Morpho rates are often higher:

- More efficient capital matching between lenders and borrowers

- Lower protocol fees compared to larger competitors

- Curated vaults managed by risk experts optimize allocation

- MORPHO token incentives add to base yield

The interface is clean and the risk management is solid — each market on Morpho Blue is isolated, meaning a problem in one market doesn’t cascade to others. That’s a smart design choice that I wish more protocols would adopt.

Verdict: Best for yield-maximizers who want higher rates than Aave/Compound with comparable security. Slightly more complex, but worth learning.

#5 Euler Finance — The Comeback Kid

Euler Finance had one of the most dramatic stories in DeFi history. In March 2023, it suffered a $197 million flash loan exploit — one of the largest DeFi hacks ever. Most protocols don’t survive something like that. But Euler did something remarkable: the hacker actually returned most of the funds, and the team rebuilt from scratch.

Euler V2, launched in 2024, is a completely redesigned protocol with modular architecture and significantly improved security. The team brought in top-tier auditors and implemented multiple layers of protection. I’ll be honest — I was skeptical at first. But the TVL has been growing steadily, and the rates are genuinely competitive.

What makes Euler V2 interesting is its modular vault system. Different risk managers can create customized lending markets with their own parameters. It’s more flexible than Aave or Compound, which appeals to more sophisticated DeFi users.

Verdict: Higher risk tolerance required given the history, but the rebuilt protocol is impressive. Good for experienced DeFi users looking for higher yields on a wider range of assets.

#6 Spark Protocol — Aave’s Little Sibling

Spark Protocol is built by the MakerDAO/Sky team and is actually a fork of Aave V3. It’s designed to work seamlessly with DAI and the broader Maker ecosystem. The rates on Spark are often subsidized by Maker governance, which means you can sometimes find better rates here than on Aave itself.

The DAI supply rate on Spark has frequently been higher than the DSR, making it an attractive option for DAI holders who want to maximize yield. And because it’s built on Aave’s battle-tested codebase, the security profile is strong.

Spark is available on Ethereum mainnet and Gnosis Chain. It’s not the most exciting platform on this list, but “boring and reliable” is actually a compliment in DeFi. I’ve had funds sitting in Spark for months without a single issue.

Verdict: Excellent for DAI/USDC lending with Maker ecosystem integration. Safe, reliable, and often offers competitive rates due to Maker subsidies.

Comparing Interest Rates: A Side-by-Side Look

For a deeper head-to-head analysis of the top three protocols, see our Aave vs Compound vs MakerDAO comparison.

Let me put the numbers in one place so you can see how these platforms stack up. Keep in mind these rates are dynamic and change constantly based on market conditions. Always check the current rates directly on each platform before depositing.

- Aave V3 (Arbitrum): USDC ~5-7%, ETH ~2-3.5%

- Compound V3: USDC ~4-6.5%

- MakerDAO DSR/SSR: DAI/USDS ~5-8%

- Morpho Blue: USDC ~6-9% (varies by vault)

- Euler V2: Varies widely by asset, often 5-10%+

- Spark Protocol: DAI ~5-7%, USDC ~4-6%

One thing I always tell people: don’t just chase the highest number. A platform offering 15% APY on a random token is not the same as Aave offering 6% on USDC. The risk profiles are completely different. Stablecoin lending on established protocols is about as close to “safe” as DeFi gets — and even then, smart contract risk is always present.

Key Risks to Understand Before You Lend

Before depositing a single dollar, it’s worth reviewing the 9 critical DeFi risks every investor must know — smart contract exploits, oracle manipulation, and liquidation cascades can all affect lending protocols.

I’d be doing you a disservice if I didn’t talk about the risks. DeFi lending is not a savings account. Here’s what can go wrong:

- Smart contract exploits: Even audited protocols can be hacked. Diversify across platforms.

- Liquidation risk (for borrowers): If you’re borrowing against collateral, a price drop can trigger liquidation.

- Stablecoin depeg risk: USDC briefly depegged in March 2023. It recovered, but it was stressful.

- Governance attacks: Malicious governance proposals can drain protocol funds.

- Oracle manipulation: Price feed manipulation can cause incorrect liquidations.

- Regulatory risk: DeFi regulation is still evolving globally.

My personal rule: never put more than 20-25% of my crypto portfolio into any single DeFi protocol. Spread it around. And always use funds you can afford to have locked up or, in a worst case, lose. That’s not pessimism — that’s just smart risk management.

How to Get Started with DeFi Lending Today

Alright, you’re convinced. You want to start earning interest on your crypto. Here’s the practical step-by-step:

- Get a non-custodial wallet: MetaMask is the most popular. (See our guide on the best wallets for DeFi passive income.) Download it, write down your seed phrase, store it offline.

- Buy crypto on an exchange: Coinbase, Kraken, or Binance. For stablecoin lending, buy USDC or USDT.

- Bridge to a Layer 2 if needed: For Aave on Arbitrum, use the official Arbitrum bridge to move funds from Ethereum mainnet.

- Connect your wallet to the protocol: Go to app.aave.com (or your chosen platform), click “Connect Wallet.”

- Deposit your assets: Select the asset, enter the amount, approve the transaction, confirm the deposit.

- Monitor your position: Check in weekly. Watch for rate changes and any protocol news.

Start small. Seriously. Put in $100-200 first, get comfortable with the interface, understand how the interest accrues, and then scale up. There’s no rush. The protocols will still be there next month.

Frequently Asked Questions About DeFi Lending Platforms

What is the best DeFi lending platform in 2026?

Aave is widely considered the best overall DeFi lending platform in 2026 thanks to its deep liquidity, multi-chain support (Ethereum, Arbitrum, Polygon, Optimism, Base), strong audit history, and user-friendly interface. For users chasing the highest stablecoin APY, Morpho often delivers 1–2% better returns than Aave or Compound on the same assets.

Which DeFi platform offers the highest interest rates?

Rates fluctuate constantly, but Morpho consistently ranks among the highest-yielding lending platforms for stablecoins like USDC and DAI because of its efficient peer-to-peer matching layer. Euler Finance and Spark Protocol also regularly offer competitive rates. Always check live APY on each protocol before depositing.

Is DeFi lending safe?

DeFi lending carries real risks — smart contract exploits, oracle failures, stablecoin de-pegs, and protocol insolvency. Established platforms like Aave, Compound, and MakerDAO have strong track records and multiple audits, but no platform is 100% safe. Never deposit more than you can afford to lose, and diversify across protocols.

How much money do I need to start DeFi lending?

You can technically start with as little as $50–$100, but gas fees on Ethereum mainnet can eat into small deposits. For amounts under $500, use a Layer 2 like Arbitrum, Polygon, or Base where transaction fees are pennies. Aave and Compound both support these networks.

Do I pay taxes on DeFi lending interest?

In most jurisdictions, yes — interest earned from DeFi lending is typically treated as ordinary income at the time it is received. Rules vary by country, so consult a crypto-savvy accountant in your region.

What’s the difference between DeFi lending and a savings account?

DeFi lending usually offers significantly higher yields than a traditional savings account, but without FDIC insurance and with added smart contract and market risk. For a side-by-side comparison, read our breakdown of DeFi staking vs savings accounts.

Can I lose money lending crypto on DeFi platforms?

Yes. Losses can occur from smart contract hacks, stablecoin de-pegging, protocol insolvency, or — if you borrow against your deposit — liquidation during sharp market moves. Pure lending (no borrowing) on audited platforms like Aave carries lower risk but is never risk-free.

Conclusion: Where Should You Start?

After all this, here’s my honest recommendation: if you’re new to DeFi lending, start with Aave V3 on Arbitrum. It’s the most trusted protocol, the interface is user-friendly, the gas fees are low on Arbitrum, and the rates are competitive. Deposit USDC, watch your balance grow, and get comfortable with how it all works.

Once you’ve got the basics down, explore Morpho for potentially higher yields, or the MakerDAO DSR if you prefer the simplicity of DAI. The beauty of DeFi is that you’re not locked in — you can move your funds between protocols as rates and conditions change.

The DeFi lending space in 2025 is more mature, more secure, and more accessible than ever before. The days of wild west 1000% APY schemes are largely behind us (mostly). What’s left are real, functioning financial protocols that can genuinely help you grow your crypto holdings over time.

Have you tried any of these platforms? Drop a comment below and let me know which one you’re using and what your experience has been. I read every comment, and I love hearing from people who are actually out there putting this stuff into practice. And if you found this guide helpful, share it with someone who’s been asking you about DeFi — let’s help more people understand how this stuff actually works.